MiCA is now operational across the European Union, marking a milestone in digital asset surveillance. Industry participants currently operate under an EU-wide framework covering stablecoins, token issuance, and services such as storage and exchange.

As the Bretton Woods Committee wrote, this process involved years of consultation and negotiation, resulting in a rulebook that addresses oversight gaps and promotes transparency.

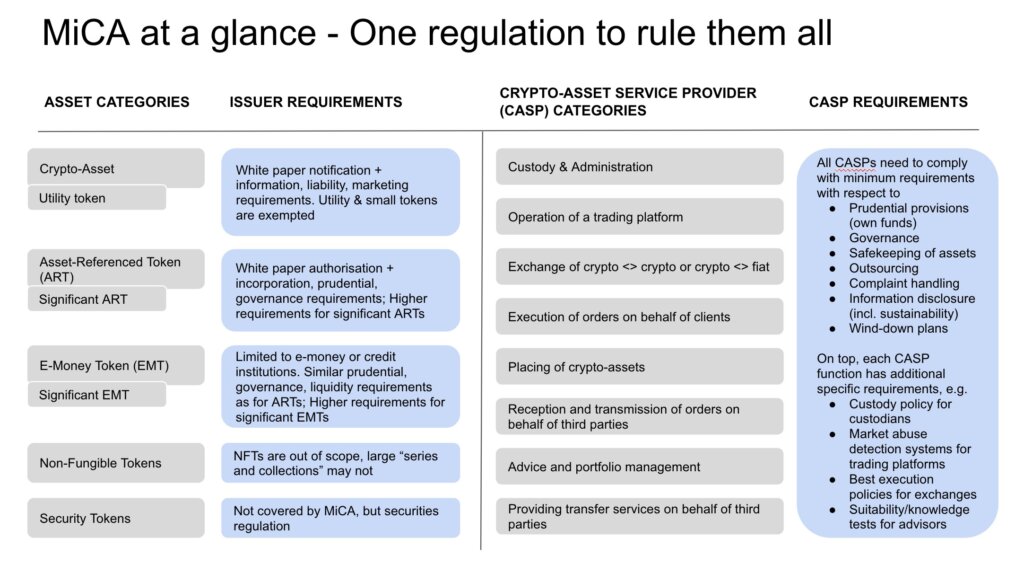

Companies issuing electronic money tokens (EMTs) must be incorporated in the EU or hold a relevant electronic money license. Asset reference tokens, on the other hand, face higher disclosure and governance requirements once they reach a certain volume or user threshold. The measures also include stricter rules on reserve management, redemption and disclosure, demonstrating the EU’s focus on financial stability in digital asset markets.

Patrick Hansen, policy director at Circle, wrote an extensive article explaining how stablecoin issuers have little choice but to comply or lose access to the entire EU market. Tether, one of the world’s leading stablecoin issuers, has chosen the latter option, telling CryptoSlate that competitors are frustrated by the company’s different approach to stablecoins. he said:

“Every day I wake up and scratch my head and I can’t understand why these two Italian guys are doing a much better job than me. Of course it’s frustrating, right?

So if your business model is called Kill Tether, you need to rethink your product. ”

Expectations for EU virtual currency companies

Once licensed in one jurisdiction, crypto asset service providers (CASPs) offering activities such as intermediation, exchange, and custody face licensing requirements that allow them to operate in all member states. The move will replace the previous patchwork of domestic regulations, reduce barriers for companies seeking cross-border growth, and introduce passport-like mechanisms similar to the approach used in traditional EU financial services. Provide.

Compliance obligations can be difficult to meet for smaller ventures, so we expect some companies to consolidate or build partnerships. Trading platforms must also establish controls against market abuse and insider trading. Authorities may prohibit the offering of tokens if disclosure or risk management procedures appear to be incomplete.

Although MiCA officially excludes from its scope protocols that are performed in a “fully decentralized manner,” many operations may not meet the threshold for true decentralization.

Similar ambiguity exists regarding large-scale NFT collections, which may be treated as fungible in regulations and require compliance with white papers and issuer obligations. There is also uncertainty regarding “privacy coins”, which could face delisting if it turns out that it is impossible to fully identify the owner.

Overall expected impact of MiCA

Industry responses from Bretton Woods and Circle indicate a common view that the practical success of MiCA depends on its technical standards and enforcement practices. Companies are adjusting their product offerings with a focus on clarity of disclosure and compliance with rules for token issuance and reserve management. As Hansen observed, adoption of this framework could attract projects seeking certainty, especially if concerns about enforcement actions elsewhere persist.

There are broader questions regarding global adoption. The United States has yet to formalize stablecoin regulations, and enforcement patterns, while seemingly progressive, vary widely across Asia. The European model could also influence other jurisdictions, encouraging a “race to the top” in consumer protection and alignment with international standards.

According to Bretton Woods, the collaborative approach will promote stablecoin passportability and reduce the risk of regulatory arbitrage. Some lawmakers are discussing MiCA 2.0, suggesting that non-fungible tokens, DeFi, or additional technical features could eventually be revisited under the updated directive. I am. Officials note that any new legal changes will depend on the initial outcome of the law.

Mr. Hansen pointed to MiCA’s similarities with other EU technology initiatives where region-wide standards ultimately influenced commercial and legal frameworks abroad. Whether MiCA becomes the default global standard will depend on its real-world implementation, the role of state institutions, and how effectively the measure protects markets while enabling companies to innovate. Meanwhile, companies continue to move to secure MiCA licenses, with major banks and exchanges adjusting their lines of business or acquiring smaller companies.

Many hope that MiCA will bring more institutional involvement with uniform licensing and consumer protection. However, the cost of compliance remains a factor that may drive activity to well-capitalized platforms. Investors may see regulated services being introduced more broadly, while smaller teams may focus on areas of expertise or relocate to regions with less stringent mandates. Policymakers believe that a unified EU stance on cryptocurrencies could strengthen capital formation and user protection, and have pledged to closely monitor the outcome.

Once this framework is implemented, stablecoin issuers and CASPs will face earlier implementation deadlines than other market participants, while the remaining rules will be phased in over the course of the year. The regulator also plans to issue binding implementation standards that will clarify the schedule, technical disclosures, and operating conditions for token projects.

Hansen acknowledged that companies planning to navigate the European situation are working with authorities and preparing their compliance strategies accordingly. He said MiCA has created an environment of clear accountability for its participants, and its ability to foster responsible growth under consistent rules will be a measure of how MiCA shapes the crypto market. I believe.

The introduction will continue in stages as the EU refines its technical guidelines and supervises licensed entities. The results will reveal whether MiCA is a viable model that balances innovation and oversight.

mentioned in this article

Arabic

Arabic Chinese (Simplified)

Chinese (Simplified) Dutch

Dutch English

English French

French German

German Italian

Italian Portuguese

Portuguese Russian

Russian Spanish

Spanish